Student loans. A heavy financial burden for many that make true financial freedom feel impossible. Even with consistently paying $218.70 a month I never felt my $21,000 student loan balance got any smaller. So I made the difficult decision to leave San Francisco in 2015 and work on becoming debt free.

It’s been a challenging two years and I wanted to give up many times. But as of April 28th, 2017 I’m living debt free. To help others I’ve assembled 23 tips I used to crush $15,000 in student loan debt (+interest) in seven months. Read below to see how I did it.

BEFORE YOU START

1. Know your estimated payoff date and find out how to shorten it

I did the math and if I didn’t start paying more than $218.70 a month I’d be in debt until 2023. I knew it felt impossible to pay more than the minimum student loan payment by moving out of Wisconsin. So I didn’t move to more desirable areas like California, New York and Seattle after Chicago didn’t work out for me. So before you start your own rapid student loan payment plan use this estimator to find your payoff date. Then figure out how to shorten it.

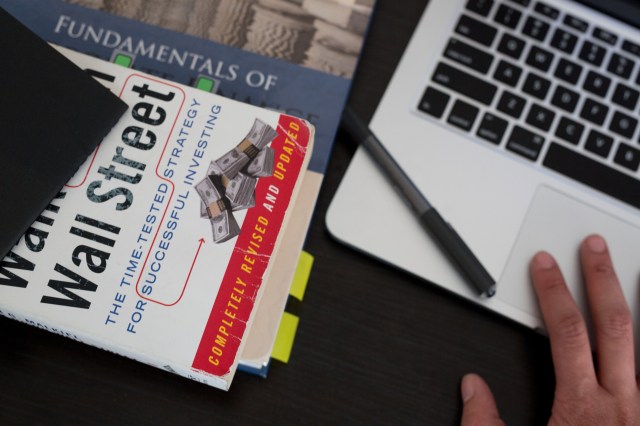

2. Set a monthly target and hit it every month

My $1,500 student loan payment target.

The more you pay each month the sooner you’ll live debt free. I wanted to pay $2,000 to $3,000 a month but that’s not realistic so I settled for $1,500 a month. I made sure I hit that target every month. It didn’t start out that way though. I paid $50 a month extra. Then $440 a month until I reached my goal of $1,500 a month. I wanted to do more, but I told myself wait until your bank account surpasses your student loan balance to make the giant payments. Once April rolled around I made a $5,833.13 payment and wiped away my debt for good with $160 to spare. I thought I’d do it in September, but I ended up paying my student loans off four months earlier than expected.

3. Create a Mint account

It may seem like a real pain to track your money, but doing so makes you more conscious of your spending. So consider Mint and other finances apps to track your spending. The envelope strategy is a good idea too.

4. Read Student Loan Hero for motivation and inspiration

Reading stories of others who paid off way more student loan debt than me motivated me to pay off my own. I found people whose student loans balance skyrocketed up to $129,000 and they paid it off in five years. So, if you feel bad about your student debt read some of these stories to boost your spirits. No matter how bad your financial situation feels it’s likely someone started out worse than you did. And if they’re living debt free why can’t you?

5. Become a finance expert

Reading about finances isn’t very fun, but it’s a good idea to read up on the topic so you don’t make costly mistakes. Check out I Will Teach You to Be Rich by Ramit Sethi. His book is great and his blog contains a lot of helpful advice. I also like Lifehacker’s Two Cents, NerdWallet and The Penny Hoarder website. And don’t forget to check out Napoleon Hill’s famous Think and Grow Rich. As well as David Ramsey’s legendary debt snowball method and Warren Buffet’s financial tips. All these resources help you look at finances in a new way and get serious about managing your money.

MISTAKES TO AVOID

6. Don’t do forbearance unless it’s absolutely necessary

If you’re unable to make your monthly student loan payments forbearance isn’t a bad option for a temporary fix. With forbearance, you don’t make payments, but your interest rolls over each month. I ended up paying more than $1,000 extra because I neglected my student loans until I got the “perfect job”. So consider forbearance if you’re in financial danger, but go back to a regular payment plan ASAP.

7. Don’t settle for making only the smallest monthly payment

I never made a late payment, but for too long I only paid the smallest monthly payment of $218.70. If I didn’t get serious and started paying more each month it would take me until 2023 to pay off all my student loans. Remember the more you pay each month the less interest you’ll pay in the long run. Even if it’s only $50 extra a month do whatever it takes to increase your monthly payment. You’ll save yourself thousands of dollars in interest payments.

8. Don’t forget to refinance your loans

A 5.8% student loan interest rate isn’t too bad, but I considered refinancing my loans. Since I paid my loan off fast I didn’t do it. It’s a great option though. Since your interest rate often drops below 2%. Many banks and credit unions offer this service so take advantage of it. Especially if you’re planning on paying off your loans for a long time. The downside? Refinancing your student loans usually means it’s difficult to change your payment plan. So before committing to it make sure you’re financially stable first.

9. Don’t forget to set up automatic payments for lower interest rate

A .25 percent reduction doesn’t sound like much, but if it’s going to take you awhile to pay your student loans off it’s worth it. I procrastinated on this because I found myself between jobs without work, but it’s a good idea. And even if you only set up the smallest automatic payment it adds up. Just remember to make extra monthly payments to pay off your student loans faster.

10. Don’t neglect your 401K, savings account and emergency fund

Carrying a staggering amount of student loan debt? If that’s the case, then it’s best to invest most of your extra income somewhere else. Why? When you’re in your 20’s and 30’s your retirement account contributions matter more now than later. The same amount you contribute in your 40’s and 50’s won’t match what you put in when you’re younger. Even though retirement seems far away don’t forget to contribute to your 401K or Roth IRA.

And don’t forget about building yourself an emergency fund either. If something unexpected comes up, you need to prepare for the worst. So pay off your student loans as fast as possible. But don’t do so at the cost of not contributing to your retirement account, savings account and emergency fund.

BIG TIPS TO GET OUT OF DEBT FASTER

11. Consider moving back in with your parents

The easiest tip and the most painful tip to do. A tough decision at 29, but I decided to swallow my pride and live at home to pay off my student loans faster. That way I easily put $1,500 a month towards my student loan every month. Plus, I didn’t need to worry about any other expensive living expenses. Like groceries, the internet and other utility costs. As a result, I paid off $15,000 in student loans (+ interest) in seven months. Not an option for you? Then get some roommates or rent out a room to decrease your rent.

12. Live away from the city or popular areas

It was tough to leave San Francisco, but it’s not going anywhere.

Living in a city rocks if you’re a young millennial. But it places a burden on your finances if you’re not careful. So, consider living out of the city for a financial break. You’ll often save on rent and it’s easier to avoid all the distractions and impulse buys from the city. It’s possible to find good deals in the city though. You’ll just want to look at less desirable areas for cheaper rent.

For instance, when I lived in San Francisco I lived in the Excelsior District. Not the most exciting area, but I didn’t pay out the nose for rent and other living costs either. If I chose more popular areas like the Mission and North Beach, I would run out of cash fast. And although my commute into San Francisco took time, I still lived in the city without breaking the bank.

13. Know your weaknesses and address them

Most of my disposable income goes to videogames and food. That said I’ve found ways to limit my spending on both. Many people consider videogames an expensive hobby, but it’s not if you’re smart about it. Instead of spending $60 on a brand new game. I spend $16 a month on GameFly and rent new releases. I also follow Cheap Ass Gamer and Wario64 on Twitter to get notified on price drops. In fact, I rarely buy a game for over $20 these days and instead opt to wait until it’s cheaper.

For food, I read food blogs, use coupons, buy in bulk, make my own meals and limit fast food to once a week to save money. Keep in mind eating out and buying drinks isn’t a bad thing if you track your spending. And if you find creative ways to indulge. Such as choosing fast food options like Chipotle, Chinese food and $5 deals that fill you up. Plus, you’ll often get two meals out of these orders. Making it a viable option in the long run and you’ll feel less inclined to eat out more than once a week.

So, figure out where most of your money goes and find a way to cut the cost or reduce it.

14. Work smart, not hard, but do work very hard for short periods

For obvious reasons you want to work the job that pays more, but sometimes that’s not always an option. And it’s possible to make more money by juggling two or three jobs instead. That’s what I did from November 2016 to January 2017 and again in March 2017 to April 2017.

Working three jobs seven days a week along with 18 hours of driving may sound crazy. But I wanted my student loans gone by 2018 so I made the sacrifice. Having three paychecks made a big difference when making student loan payments.

I found working every day easier than working the same type of jobs M-F. Working 8- 12 hour days not too bad every day. But working 16 hours M-F even with weekends off not so much fun. The variety of jobs helps too. I didn’t mind doing sales work and talking to people after doing factory work.

Not thrilled about working overtime? Just remember it’s only temporary. It’s a lot easier to get through a long work week if you know ahead of time when the job ends. For example, I did a 10-week job with Microsoft as a brand ambassador so I knew it didn’t mean forever which kept me going.

15. Be ready for roadblocks

My temporary job with Microsoft paid well to justify the long commute, but I didn’t drop my other jobs that paid less. That way I prepared myself for the financial hit when the job ended. Which meant keeping up my $1,500 a month student loan payment plans a non-issue. But don’t feel bad if you struggle one month and can’t hit your target. Instead, try to hit it next month or close to it until you get your monthly income back on track.

16. Delay gratification

The other hardest tip besides living with your parents. I wanted to throw in the towel and move back to San Francisco so many times, but I didn’t. I passed on applying to dream jobs because I knew I’d only make $218.70 monthly student loan payments if I moved. I made a commitment to paying off my student loans and I intended to finish what I started.

To fight the depression, I visualized a life without debt. Mentally said over and over again it’s only temporary and kept going. I remembered what a neighbor told me in San Francisco that the city isn’t going anywhere. But your student loans won’t go away on their own.

No matter how bad it got I remembered by paying $1,500 each month I saved myself years of being in debt. I actually looked forward to seeing $1,500 go away each month from my bank account. Because each payment meant seven months without debt. Remember your situation is only temporary. So repeat the words “I’ll handle it” again and again until you believe it.

IF YOU CAN’T FIND A JOB IN YOUR FIELD OR NEED EXTRA INCOME

Can’t find a full-time job in your field? It’s one of the most frustrating feelings after graduating college. Not to mention you’re stuck with expensive student loans to pay off. Luckily, your major doesn’t dictate your fate. So if your major isn’t working out then get a job outside your field. Yeah, it’s not what you want to do. But it’s better than starving yourself, not paying your bills and filing bankruptcy.

In a similar situation? Look below for some work ideas I used when writing full-time didn’t work out for me.

17. Some temporary job ideas

These work whether you’re looking for work or want to boost your monthly income. Plus, they pay better than minimum wage jobs and a degree isn’t required. So consider these until you get the job you want. Or as another part-time job besides your main job. And don’t feel ashamed to take any of these jobs because you think the work is beneath you. Sometimes you have to do things you don’t want to survive.

One thing to keep in mind though. Don’t list them on your resume or LinkedIn when applying for jobs in your desired field. It reflects poorly on you if you include irrelevant jobs outside of your field. Also, it’s worse than gaps on your resume. If an employer in your field asks about employment gaps just say you did these jobs to pay the bills. But leave them off your resume and LinkedIn unless it’s relevant to the job you want.

Security guard

My first job out of college. I spent most of the time patrolling a college art dorm and writing hourly notes. It paid pretty well and if you take more training classes your pay rate rises above $20hr. Another great perk for me included ample time to pursue freelance writing work. Some companies won’t allow electronic devices, but take advantage of your downtime if they do. It’s easy to work on some paid contract work or take online classes between your patrols and hourly notes.

Brand ambassador

Often pays double what retail does and you don’t need to use the cash register. Plus, some companies offer commission, quarterly bonuses and deep discounts on products. It’s a hard job to find full-time since most positions favor seasonal or part-time workers. However, it’s easy way to make some extra money on top of your existing full-time job. Or a great temporary job while you look for something more permanent.

Factory worker

One of the fastest ways to pay off your student loans. You make good money doing overtime along with great benefits like health insurance. Work with a Union if possible though. I worked at a clothing, cheese and plastic factory and the latter had the best benefits because of the Union. The work gets boring. But with overtime, I made $24hr and $32hr on Sundays. And if you get it regularly with just an extra eight hours a week it’s possible to add $250 to your weekly check. Also, sometimes it’s not a bad idea to work a boring job. So you can have more time to focus on your passions, career goals and hobbies.

Conference event staff

A great place to network and make contacts to help you advance in your career. I volunteered for VentureBeat conferences and wrote articles on the GamesBeat community page. The experience helped me get hired at a tech PR agency and as a coauthor on a eBook for TapSense. Later I worked for a staffing company and made $400 bucks for two days of work. Like brand ambassador jobs most of the jobs only offer part-time hours or seasonal positions. But if you get them it’s a good source of extra income.

Temp agency

Already work full time? Consider a temp agency where you work once or twice a week. It’s an easy way to add an extra $60 to $200 a week. I worked at a cheese factory once a week and got paid $13hr to put cheese in a box and make boxes. I liked working there. Plus, I got free fresh mozzarella cheese to take home weekly. The money added up and I kept doing even after I paid my loans off for more income.

Remote work

No jobs in your area or live too far away from the city? Do your best to freelance your services to others in cities on Craigslist. Or look for contract work on AngeList and email people. A good way to build your resume and get hired full time later.

Costco

I worked at Costco as a brand ambassador for Sony and enjoyed working with the staff. Very friendly people who received great benefits. Like 401K match and shift premiums for working Sunday. I also liked that I got a free lunch every weekend I worked there because of the food samples. And I respect Costco for not forcing their staff to work on Thanksgiving. A rarity among retailers. So, if your job options feel limited then consider Costco. Finally, not surprising, but Costco received the best place to work this year from Forbes.

LITTLE TIPS THAT HELP

18. For holidays ask for gift cards or student loan payments

When my birthday and Christmas came around I didn’t request new video games or other gifts. I asked for gift cards so when new video games released next year I could use the cards instead of my cash. That way the cash I’d normally use on new games went to my student loan payments instead.

19. Use those credit card rewards

Guilt free spending at its finest. Everything here bought with credit card rewards and Amazon gift cards.

Everyone uses credit cards, but do you take advantage of your rewards? The more you use them for everyday purchases and monthly bills the more you build up points or cash. So practice some self-discipline and don’t buy those expensive purchases until you accumulate enough cash or points. Some good cards I use include the Amazon Prime Reward Visa Signature Card and Discover Card. I get 5% back on select purchases with both of these cards.

20. Use your tax return towards student loans

I got a bigger tax return than I expected this year so I used it to pay off my student loans early. With the money saved up from working three jobs and the $1,500 from my tax return, I made a student loan payment of $5,833.13. Paying almost four times what I paid in the previous four months. So when tax season rolls around resist the temptation to use it for your wants and put the money towards your debt. Think about it. By making one giant student loan payment once a year you’ll knock a year or more off your debt.

21. Make as many sacrifices as possible

I avoided bars, frequent trips to Madison and opt to stay home most nights. I didn’t go to expensive video game or anime conventions which I enjoy. I didn’t get a smartphone and stuck with a boring flip phone. Didn’t subscribe to Netflix. Did my best to limit fast food to once a week. Forgot about the gym membership and worked out at home. Didn’t see most new movies opening night and went to a Saturday morning matinee instead.

You get the idea. Think of ways to cut back and save that extra money for student loan payments. Here’s a list for some ideas that help. But like Ramit Sethi from I Will Teach You to Be Rich says make sure you focus on the big wins first.

22. Try your luck at the casino and lottery tickets

Not a bad day at the Casino.

It’s possible to make good money if you gamble smart. I won $304.95 at the slot machines and a few bucks off some lottery tickets. Keep in mind games like blackjack and craps result in better luck in your favor than the slot machine. But you never know when you’ll get lucky. So don’t feel guilty about visiting your local casino to win some extra money.

Be responsible for your gambling and lottery ticket buying though. You don’t want to turn into the Twilight Zone guy. I set a restriction of once a month or every other month and a $40 limit. I view it as entertainment like going to movie or concert. I also only buy lottery tickets when the jackpot’s high and every other time I fill up on gas.

23. Sell your unused goods online

I’ve written about eBay, Craigslist and Amazon before so no need to reiterate. There’s treasure everywhere in your room. So get rid of some of your unused belongings for cash. Spend an hour or more on the weekend making listings and keep it up every week. The extra cash adds up.

WHEN THE BIG DAY ARRIVES

First off congratulate yourself! You’ve accomplished something most people take decades to do. Treat yourself to a nice dinner or a special gift. I went out for Mexican food with my parents and bought a Nintendo Switch to celebrate being debt free.

So you’re out of debt now what?

Use that extra money from your paychecks and invest in your future. Put more money in your 401K, Roth IRA, savings account and resolve never to get into debt again. Finally, share your story and help others around you achieve financial freedom too.

Student loans feel like a big bag of bricks on your back that never goes away. However, with some determination and hard work, it’s not impossible to get rid of them. Not all these tips apply to everyone. But I hope anyone who reads this blog post finds some way to rid themselves of their student loans for good. I’ve shared my story. Now it’s up to you how fast you pay your student loans off. Best of luck and remember not to give up no matter how hopeless your situation is. If I can do it so can you.

Awesome, tips!